Planet Labs: Inaccurate Forecasting and Slowing Growth

We’re either completely alone in the universe or we’re not. Either outcome is equally terrifying, so it’s best not to think about that stuff too much and stay focused on stonks. Planet Earth is our only home, and understanding it through imagery is now possible thanks to geospatial intelligence vendors like the aptly named Planet Labs (PL).

Why We Invested in Planet Labs

Our thesis was simply this. Most NewSpace themes are low-margin, capital-intensive ventures that don’t offer software-like gross margins. Planet Labs was an exception to that rule with their “capital light” geospatial intelligence business that’s a cut above the other pure-play publicly traded geospatial intelligence companies out there. We invest in leaders, and Planet Labs leads in terms of revenues and market cap when compared to other pure-play geospatial intelligence stocks.

Then the problems started. First, we noticed it in the proprietary metric Planet introduced called “winbacks.” This was supposed to measure customers whose contracts lapsed, then salespeople chased them down to resubscribe. If Planet’s solution is so valuable, then people should be proactively renewing their contracts instead of having to be chased. In their recent earnings call, the company cites seasonality as an explanation for “gaps between when a contract expires and when the customer focuses on the renewal.” Fair enough, so we can look at net retention rate (NRR), something that has been volatile and ended this year at a dismal 101% (partially explained by contractions of certain contracts with customers in the commercial vertical). In other words, existing customer spend didn’t even increase enough to make up for inflation, though we’re told it’s “not indicative of higher churn” which isn’t entirely reassuring. That dreadful NRR metric was overshadowed by a number of other concerns surrounding the company’s ability to grow.

Growing Pains

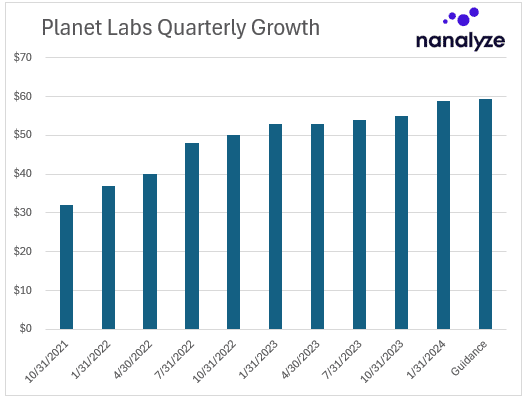

Back in the good old days, Planet exited Fiscal 2023 with an NRR of 131% and revenue growth guidance of 30% on the low end. Then this guidance changed to 18% which the company attributed to “extended sales cycles, as well as some of our larger deal opportunities closing with smaller values than anticipated.” Then the next quarter, guidance dropped again to 13% on the lower end which allowed them to “beat expectations” by finishing the year with a meager 15% compared to the 46% revenue growth they realized the year prior. What’s most disappointing is that after failing miserably all year at providing accurate annual guidance, they just decided to drop the practice entirely. As for next quarter’s guidance, it’s a meager 1% growth sequentially.

Analysts rightly questioned Planet’s decision to not provide guidance and management’s answer was shifty at best. “The fact that we do have so much opportunity that makes it hard, as opposed to the opposite,” suggests that Planet is hesitant to guide because of variability on the upside, but then in the same breath we’re told, “We’re not assuming acceleration in our year-over-year growth rate as we progress through the year.” So, it’s safe to say we should expect 15% growth this year then? Wishy-washy comments like this imply that management doesn’t have a good handle on what to expect from their business.

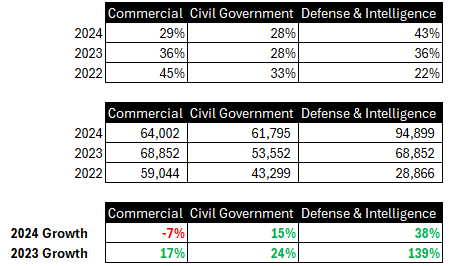

Some color can be found in looking at what’s working and what isn’t. We’re told that “revenue in the Defense & Intelligence vertical grew over 30% year-over-year, while revenue in the Civil Government vertical saw solid growth as well.” Looking at past financial statements allows us to paint the below picture of how their three segments are growing over time.

The decline in commercial revenues was attributed to budget constraints and the completion of a large legacy contract. Says the company, “There’s been a lot of pressure on the ag sector in particular, which was our biggest part of our Commercial segment and that’s had its challenges.” They go on to talk about how the long-term future is bright, and the entire earnings call points to a year where we can only hope for the 15% growth realized last year. That’s not a bad number, but it’s not the pretty picture they painted in their SPAC deck. The key takeaway here is that in just sixteen months we went from Planet Labs: Competency and Growth to Planet Labs: Inaccurate Forecasting and Slowing Growth.

Runway and Competition

The earnings call talks about “very large government customers that will look to us to sustain a nine-figure balance” of cash on the books which means the $300 million in cash they have is more like $200 million. That needs to last until they can become cash flow positive. In the earnings call, management emphasized how they planned to achieve “adjusted EBITDA profitability” by the fourth quarter of this year, and the negative operating cash flows of $51 million last year mean they have plenty of runway left. Our biggest concerns surround the company’s ability to grow into the $128 billion market opportunity they claimed was waiting to be captured.

There are two possibilities here. One, their market size forecast turned out to be as bad as their revenue guidance, or two, they’re not capturing the opportunity because their product is lacking and other competitors will eventually eat their lunch. Taking pictures of the planet is a commodity offering, but adding insights to the imagery is where the value lies. We can’t help but look at the massive constellation that Starlink has and wonder just how easy it would be for them to start adding cameras to some satellites. On the latest earnings call, one analyst probed a rumored offering from SpaceX called Starshield – “a network of hundreds of spy satellites under a classified contract with a U.S. intelligence agency,” according to Reuters. Planet’s response was that SpaceX’s venture is “very different from our business.” Famous last words?

Thoughts on Planet Labs

We exit any disruptive tech stock for two main reasons – growth stalls or our thesis changes. Regarding growth, anything in the double digits would be considered acceptable provided it has a valuation to match. As for the geospatial intelligence thesis, even if it were 10% of the $128 billion market Planet talked about there would still be plenty of upside. Planet’s simple valuation ratio of 2.5 (compared to our catalog average of 6.5) reflects the slowing growth and accompanying uncertainty surrounding their business. The first decision we need to make here would be whether to add shares at these depressed levels. If we choose not to, then it’s hardly fair that Planet Labs continue to occupy a slot in the Nanalyze New Money Report as one of the stocks we find most compelling.

When it comes to space stocks, there aren’t many to like, and we picked Planet to provide investors with some exposure to the exciting NewSpace sector. Taking a more holistic approach, there are certainly more compelling names that could occupy that slot were we to look outside of NewSpace. The next step is to take today’s findings and discuss them internally. Should we add shares, and should Planet continue to occupy a slot in our New Money Report? We’ll let paying subscribers know soon enough.

Conclusion

The biggest concern we have surrounds a management team that did an exceptionally poor job at providing guidance and then decided to give up the practice entirely. In second place would be a concern that’s persisted for a while now – Planet Labs’ solutions may not be that useful for clients who need to be convinced to continue using them (winbacks) and who are not increasing spend on the platform as time goes on (the dreadfully low NRR metrics). Falling back on the company’s SaaS roots, decent gross margins, and desirability relative to all the other space junk out there doesn’t make us feel any better. It’s time to take a long hard look at what to do with Planet Labs.